Financial formulae

Financial Calculation Formulae

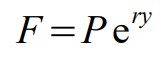

Continuously compounded interest on a fixed investment

F = Future value

P = Initial principle invested

r = Annual percentage interest rate, APR

y = Number of years invested

e = Euler’s number, 2.71828…, the base of the natural logarithm

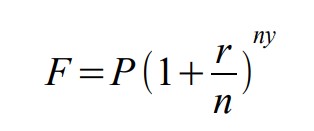

F = Future value

P = Initial principle invested

r = Annual percentage interest rate, APR

n = Number of times compounded per year

y = Number of years invested

r/n = Interest rate per compounding period

ny = Number of times compounded over y years

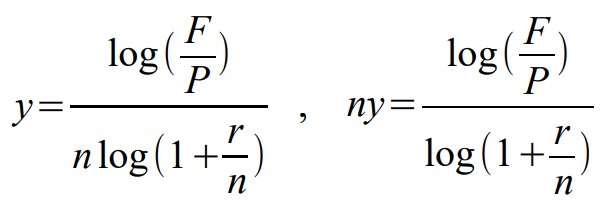

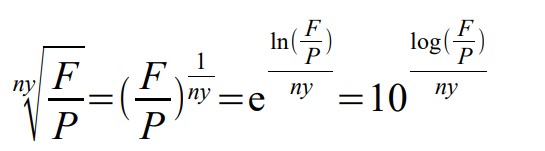

y = the number of years required to achieve a financial goal are interest rate r

ny = the number of compoundings to achieve a financial goal are interest rate r

You must round up to the next compounding to fully achieve the financial goal.

Any base log can be used, as long as you are consistent.

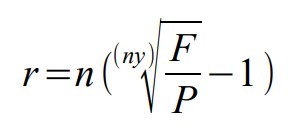

where: r = the interest rate required to achieve a financial goal in y years.

If your calculator does not have and y √ x function, logs may be used as shown above. (Any base log can be used, as long as the log and base are consistent.)

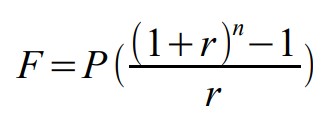

F = Future value

P = Additional principle invested every compounding period

r = Interest rate per compounding period

n = Number of times compounded

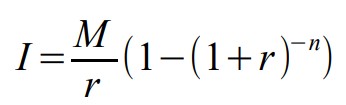

I = Initial investment required to receive n payments of M dollars

(a loan made to the bank)

M = Amount of money received from the annuity per period

r = Interest rate per compounding period

n = Number of payments received and times compounded

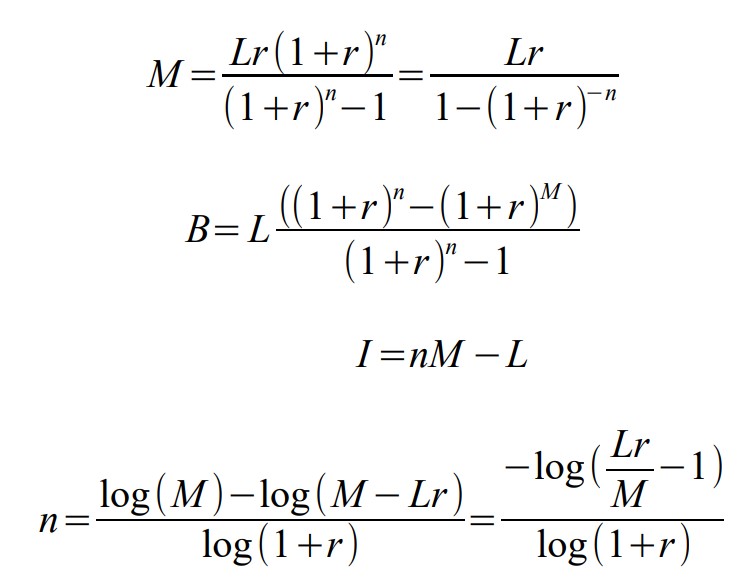

M = The periodic payments to be made

L = Initial principle of loan taken

r = Interest rate per payment and compounding period

n = Number of payments to be made

Mn = Total cost of borrowing L dollars over n payments

B = Balance due after making n payments of M dollars

I = Total interest paid on borrowing L dollars over n payments

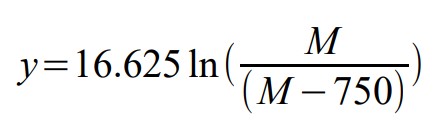

n = Number of payments of M dollars to pay off a loan of L dollars at rate r

What does capitalization of a loan mean?

Example:

- As a college student, you take out a college loan that has a non-zero interest rate, but payments need to be made for 5 years. You are deferring payment of both the initial loan and the interest.

- Every month for those 5 years, you effectively borrow more money from the lender to pay the interest on the loan and accrued interest.

- At the end of the 5 years, you now have a larger loan, which you must now pay as a conventional mortgage.

Note:

- Part 1, the first 5 years: This is treated as a saving account computation, where the initial value is the loan amount. The final value is the initial loan plus accrued interest.

- Part 2, the payoff years: This is treated as a conventional mortgage computation, where the loan amount is the initial loan plus the accrued interest.